Liu Xinnuo, CEO and Executive Director of KVB Kunlun International, delivering a speech at the 12th Asian Financial Forum

Distinguished guests, good morning everyone. I am Liu Xinnuo, CEO of KVB Kunlun International Financial Group.

The two previous speakers spoke about the sustainable development of Hong Kong and the Greater Bay Area, as well as China's macro foreign exchange policies. We also introduced, through a documentary, how KVB Kunlun International's team has been practicing inclusive finance in rural areas of mainland China.

Today, the theme of my speech is "Smart Finance for Inclusive Support of Hong Kong SMEs, Building a Sustainable Ecosystem and an Inclusive Future Together"—which is also the theme of today's conference. I will elaborate on this from three aspects.

First, practicing inclusive finance requires an original aspiration and perseverance.

Eighteen years ago, KVB Kunlun International was founded in New Zealand. From a small enterprise of fewer than 10 people, it kept growing. One could say KVB is a classic small-business startup story. Since our founding, although our annual trading volume has reached US$300 billion, and we have become the first foreign exchange main-board listed stock in the Greater China region, with tens of thousands of clients spread across the world, we still consider ourselves a small and medium-sized enterprise. In Hong Kong, our listed and non-listed companies together have only just over 80 employees. According to the definition of the Hong Kong Productivity Council, any company with fewer than 90 employees is an SME.

Because we originated as a small enterprise, throughout our entrepreneurial growth we encountered all the difficulties and hardships that small businesses face, including rejection and unfair treatment. During this process, we also received help from banks and international institutions with heart and a sense of equality, such as Citibank and PwC, among others. Without the support of these banks and institutions, we could not have succeeded. For this, we are deeply grateful.

It is precisely because of our small-business origins and this experience that serving SMEs became our original aspiration and commitment. Over nearly 20 years, we have been dedicated to serving SMEs around the world. Whether in Australia or New Zealand in the Southern Hemisphere, the Greater Toronto Area in North America, or Hong Kong and mainland China, our employees can be found serving SMEs, with many moving stories. We work diligently to meet each client's financial service needs, actively promoting the integration of financial technology with enterprise development, and providing SMEs with efficient, automated global trading and settlement. As a result, we have earned praise from all sectors and won countless awards.

Second, practicing inclusive finance requires a deep understanding of the pain points and challenges facing SMEs.

Let us look at the actual situation of Hong Kong's SMEs.

According to 2018 data from the Census and Statistics Department of the Hong Kong Government, Hong Kong currently has a total of 330,000 SMEs, accounting for 98% of all business establishments. Among them, 110,000 are engaged in import and export trade, providing jobs for more than 1.3 million people. In other words, the well-being of Hong Kong's SMEs is a livelihood issue.

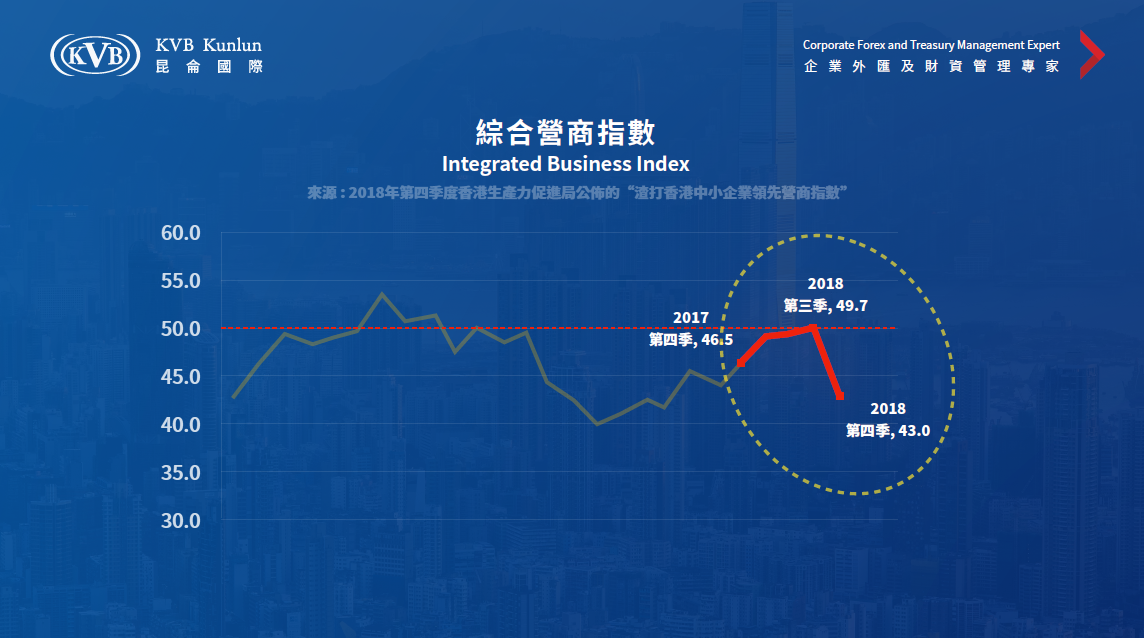

According to a special survey by the Hong Kong Productivity Council on local SMEs, in the fourth quarter of 2018, the composite business index calculated from 800 sample enterprises in manufacturing, import/export trade and wholesale, and retail declined across the board. This was mainly reflected in recruitment intentions, investment intentions, business conditions, profit performance, and the global economic situation. Among these, the fourth quarter of 2018 saw a relatively large decline compared with the third quarter. This shows that Hong Kong's SMEs are greatly troubled by the current business environment they face.

In the industry classification index, we can see that the business conditions and profit performance of import and export trade enterprises in the fourth quarter of 2018 both reached the second-lowest levels on record, with the largest decline and a straight downward trend. This shows that the industry outlook is extremely uncertain.

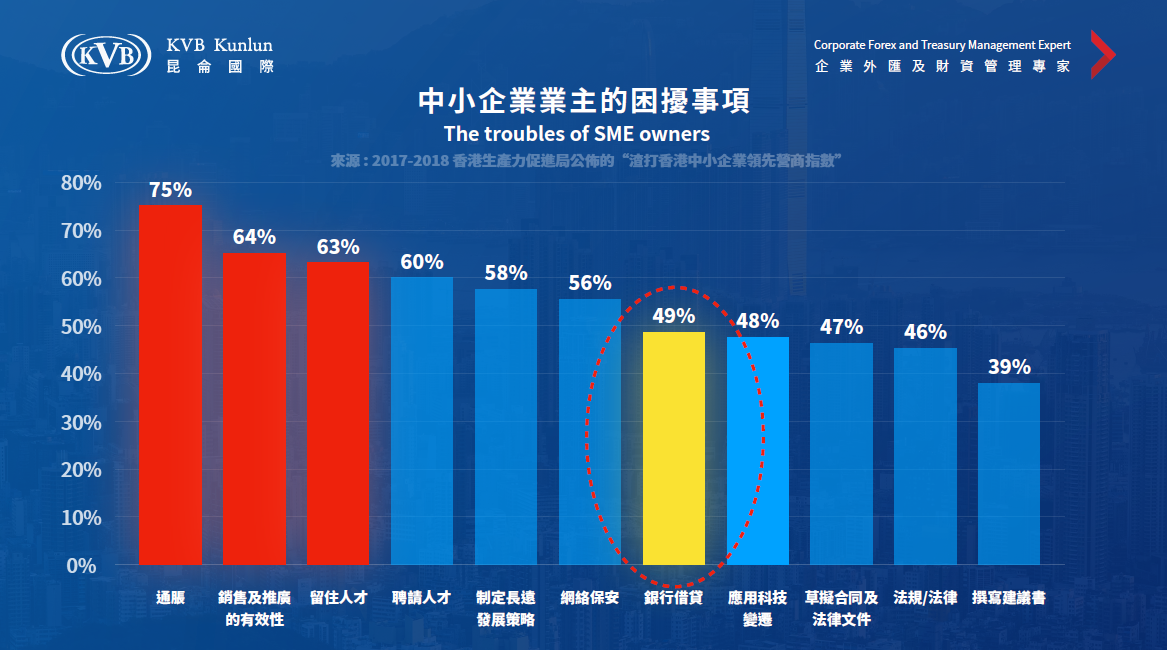

In the survey of the concerns of SME owners, we can clearly see that inflation, the effectiveness of sales and promotion, and retaining talent are the three areas that most worry SME owners. Bank lending ranked only 7th on the list, which shows that most SME owners are more concerned about inflation and cost issues rather than bank loans—or in other words, borrowing money is not the fundamental solution to the problem.

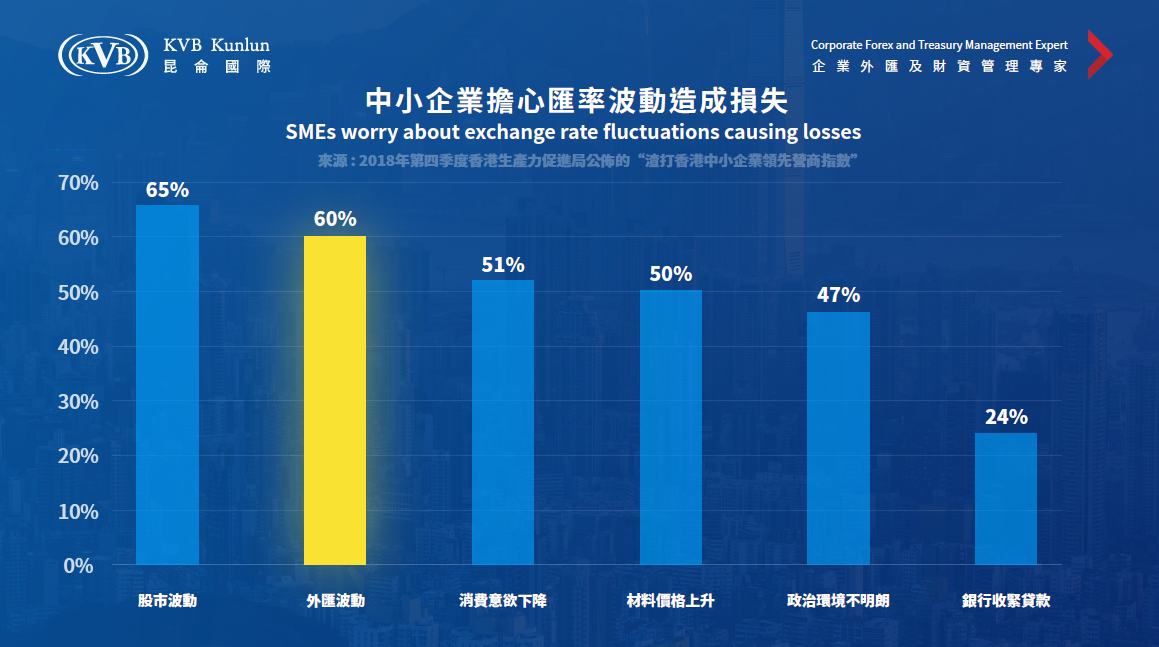

At the same time, we see that in the fourth quarter of 2018, losses caused by exchange rate fluctuations were one of the main concerns of local Hong Kong SMEs. Our guest, Dr. Guan Tao, also mentioned that in 2018 the renminbi experienced significant fluctuations of up to 4% and down to 10%, which further demonstrates SMEs' urgent need for foreign exchange services.

Faced with an uncertain economic outlook and a volatile foreign exchange market, how should our SME owners manage exchange rate risk?

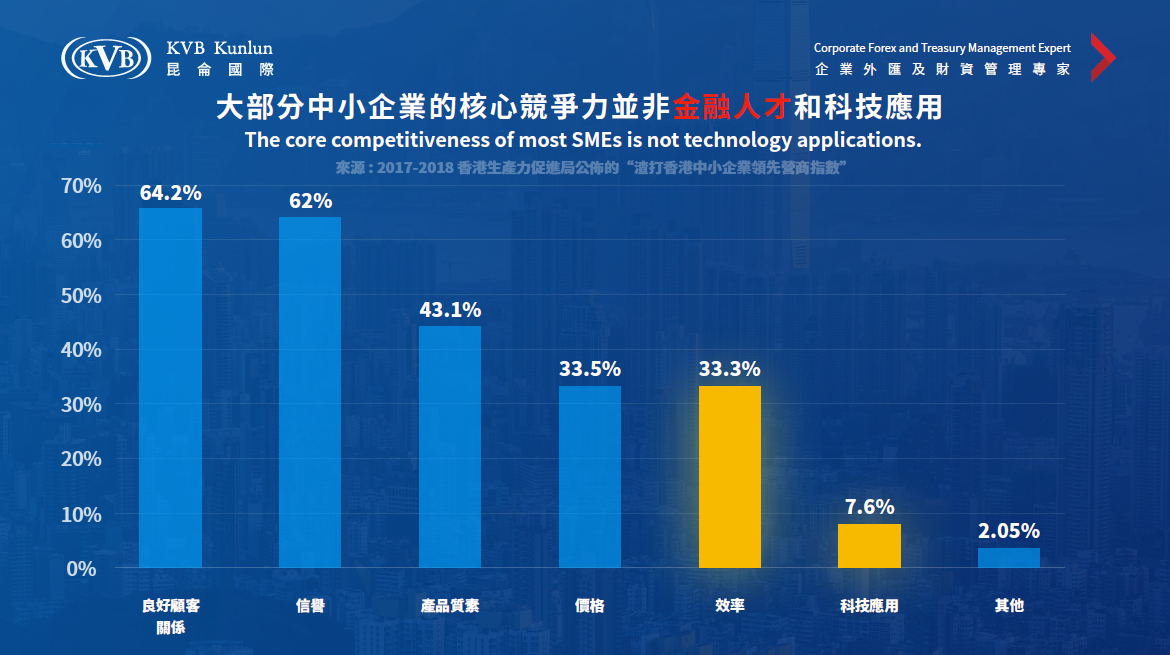

In the chart below, we find that the core competitiveness of most Hong Kong SMEs does not lie in bringing in financial talent or strengthening the application of financial technology. SMEs' investment in information technology is also clearly insufficient; they devote most of their energy and funds to maintaining client relationships, paying rent, and paying salaries. Imagine if our SME owners could obtain advanced financial technology tools at a lower price and cost, thereby enhancing their comprehensive financial soft power—would their survival and development be in a more favorable position?

The survey data above, on the one hand, reflects the challenges and uncertainties facing the future development of Hong Kong's SMEs, and on the other hand, reveals the fact that Hong Kong's SMEs generally lack support and assistance and urgently need inclusive financial technology. To practice inclusion, we must deeply understand the problems and difficulties of SMEs, so that we can prescribe the right remedy.

Third, the capabilities needed to bring inclusive finance to Hong Kong SMEs—Smart Finance!

If we truly want to help SMEs, we ourselves must have wisdom, capability, methods, and tools!

If "smart" refers to financial technology means, and "exchange" refers to foreign exchange—which is also our area of expertise—then we can say with confidence that KVB Kunlun International, once an SME itself, is now a company listed on the Hong Kong main board and the first foreign exchange stock in Greater China. Our 20 years of practical experience in the foreign exchange field, together with substantial investment in financial technology, have enabled us to grow ever stronger, possessing both hard power and soft power, and giving us the ability to help more SMEs achieve technological innovation and take off.

In 2018, we won multiple awards at home and abroad on the strength of real client service cases. Last November, we joined the Bank of China, Citibank, and three other banks as winners of The Asian Banker's "Best Transaction Bank and Solution" award. We were the only non-bank financial institution to receive this honor. This is the industry's best recognition of our service and technology.

Let me give another example. Last year, we established a business relationship with an online travel platform related to cross-border payments. Because the company was not large, its client orders were scattered, with small transaction amounts and high frequency, it had no chance of receiving the large-client service treatment offered by banks. After understanding their situation and difficulties, we used our "Smart Finance" solution to help them build an API automated trading interface, changing their original order-processing model. Using "finance + technology," we helped this SME meet its needs for hundreds of millions of foreign exchange price queries per day, exchange rate locking, multi-currency trading, and more, helping them save operating costs, improve operational efficiency, and reduce foreign exchange risk. In just one year, this company has already stood out from its competitors and is about to become a listed company.

I want to use the above case to illustrate our ability to successfully implement "Smart Finance." Using advanced financial technology means to help SMEs solve their difficulties fulfills our aspiration to create the best experience and platform for SMEs. We believe that service cases like this should not only be continuously replicated in mainland China and overseas, but also in Hong Kong and the Greater Bay Area, becoming the successful model of our Hong Kong "Smart Finance." We hope that, with the original aspiration of inclusive finance, we can bring more tangible benefits to Hong Kong's SMEs, give them support, and enable them to survive and develop better.

Having discussed the above three points, I must say that practicing inclusive finance is not easy. Inclusion is a beautiful word, but practicing it means facing many challenges and difficulties. This requires us to uphold goodwill and our original aspiration. We firmly believe that every SME should have the opportunity and right to access financial services. To practice inclusive finance, we must have the ability to stay closely connected with SMEs, to deeply understand their pain points and uncover their needs. This requires experience, combined with technological means, so that goodwill and original aspiration can be realized.

Finally, I also call on all sectors of society to jointly support Hong Kong's SMEs, to give them genuine care with an open mind, and to together create a sustainable future for them, so that inclusive finance truly benefits Hong Kong's SMEs! Thank you all!