Building an Internal, Professional, High-End Platform for China-U.S. Financial Exchange

Dialogue with Wall Street

Dialogue with Wall Street

Issue 40 (May 9, 2014)

Ba Shusong, Researcher

Email: bashusong@qq.com

New York Phone: +1(718)839-3123

(Internal exchange minutes. The discussion represents personal views only, is unrelated to the speaker's affiliated institution, and does not represent the opinion of any institution. This issue's report was jointly compiled by Researcher Ba Shusong and Dr. Niu Bokun, 13811593606, for internal reference only. Please do not distribute externally. Thank you. This report has not been reviewed by the keynote speaker.)

[This Issue's Topic]

The Advent of China's Forex Era

[Keynote Speaker]

Mr. Liu Xinnuo is Managing Director of KVB Kunlun International Group and one of the company's founders. In the early 2000s, he accurately predicted the two major macro trends of "RMB internationalization and the development of China's offshore financial markets," and based on these macro trends, he planned and implemented the Group's ten-year development strategy. To date, the company and its business have expanded to 6 international cities across 4 countries. In 2013, it became the first non-bank financial institution in the Greater China region to go public with foreign exchange trading as its core business, and one of only 5 listed forex brokers worldwide (the other four are all European and American financial institutions). Leading a global team with innovative, differentiated service concepts, Mr. Liu Xinnuo took the lead in launching various offshore RMB products and settlement services in the forex market. Drawing on high-caliber financial technology capabilities, the company undertook the development of China CITIC Bank's international forex trading platform, which passed the Hong Kong Monetary Authority's acceptance review and was successfully launched. In global competition, the company holds its own against international financial institutions. In addition to successfully obtaining various financial licenses and meeting the increasingly stringent compliance oversight of regulators in each country/region, it has maintained a record of zero penalties for over a decade. The company also strives to become a model of legal, compliant, and sound conduct for Chinese-funded financial institutions in the international financial markets.

[Meeting Minutes]

I. Review of Major China Forex Events in 2014

Since July 21, 2005, the RMB exchange rate shifted from a fixed exchange rate mechanism to a managed floating exchange rate mechanism based on market supply and demand with reference to a basket of currencies—a period of 9 years to date. In the first quarter of this year, the RMB depreciated, moving from 6.06 at the start of the year to a high of 6.26, a swing of 3%. Compared with the nearly 20,000-basis-point one-way appreciation of the RMB against the U.S. dollar over the past 9 years, the current pullback and adjustment in the RMB exchange rate is a normal phenomenon. On March 22, at the China Development Forum, Yi Gang, Deputy Governor of the People's Bank of China and Director of the State Administration of Foreign Exchange, stated: "Going forward, two-way exchange rate movement will be the norm, flexibility will increase, and the RMB exchange rate will be primarily determined by market supply and demand." In the Japanese forex market at the end of the last century, "Mr. Yen" Eisuke Sakakibara influenced the yen exchange rate through verbal or actual intervention, restraining the yen's one-way appreciation while bulls and bears sparred in the market. The China forex market over the past couple of months has had a similar flavor.

On the policy front, a categorized comparison of the number of currently effective forex management measures and regulations in China over the past three years reveals that current account forex management dropped from 141 items in 2011 to 27 items in 2013, capital account forex management dropped from 141 items to 105 items, and forex technology management rose from 0 to 4 items. This shows that forex management under both the current account and the capital account is being relaxed, while forex technology oversight has been strengthened somewhat.

In addition, the "Notice of the State Administration of Foreign Exchange on Further Improving and Adjusting Capital Account Forex Management Policies" (Huifa [2014] No. 2), issued in the first quarter of 2014, is an important measure of forex reform. It simplified many registration and approval procedures, improved efficiency, and promoted the healthy development of cross-border demand.

II. The Trend of RMB Internationalization

Looking at the ranking of global trading currencies, the Bank for International Settlements' 2013 report showed that, in terms of average daily global trading volume in 2013, the RMB's share of global forex trading rose from 0.9% in 2010 to 2.2%; the Hong Kong dollar's share of global forex trading fell from 2.4% in 2010 to 1.4%. This indicates that the trading scale of offshore RMB is continuously rising, while at the same time squeezing the trading space for the Hong Kong dollar.

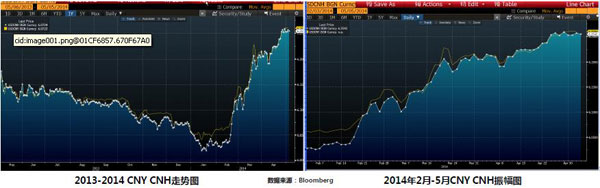

Looking at the RMB's trajectory, over the past decade or so the RMB against the U.S. dollar has only shown one-way movement. Based on the thinking of the central bank and the forex bureau, as well as market performance, this pattern will be gradually broken in 2014. Effective March 17, 2014, the daily trading band for the RMB against the U.S. dollar in the interbank spot forex market was widened from 1% to 2%. So far this year, cumulative RMB depreciation has exceeded 3.2%, drawing a strong market reaction. Large foreign banks' first-quarter forecast levels shifted to the 6.15-6.30 range. The RMB's one-way appreciation trend has come to a close and a pullback has appeared.

Looking at the offshore RMB's trajectory, the overall trend of offshore RMB remains similar to that of onshore RMB. However, as the RMB internationalization trend deepens further, with the amplitude within the onshore RMB range increasing, offshore RMB is bound to see more pronounced arbitrage uses. The chart below is a dual-currency volatility analysis through early May; there is an arbitrage space of roughly 0.1% to 0.2% between them, and there are more and more cases of hedging settlement risk overseas through offshore RMB.

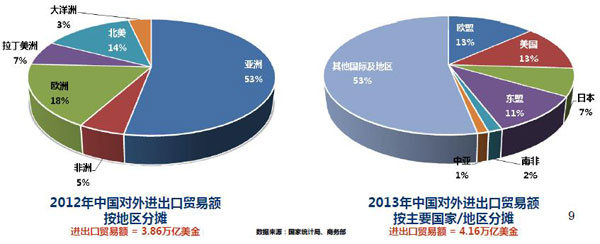

Looking at the current state of global trade, China's import and export trade volume already ranks among the top in the world, and its active trading partners have long extended beyond the traditional G7 countries. The scope for direct RMB conversion and settlement is being fully liberalized. The sum of USD-denominated China-U.S. trade and trade between the mainland and Hong Kong (where the Hong Kong dollar is pegged to the U.S. dollar) accounts for no more than 20% of China's total trade. Even when China's trade with many countries such as Japan, South Korea, Australia, Brazil, India, South Africa, and Canada is settled in U.S. dollars, the pricing currencies are all non-USD currencies, and pricing is largely tied to the exchange rate fluctuations of non-USD currencies. So behind the trade is the impact of RMB exchange rate fluctuations against these countries' local currencies. This is no longer an era of closely watching the U.S. dollar; paying attention to the RMB's movement against a basket of currencies other than the U.S. dollar is crucial.

Looking at the RMB's movement against other major trade currencies, observing the RMB's trajectory against the Japanese yen and the euro over the past 5 years, we see: the RMB is already at a historical high; as the economic conditions of the G5 countries gradually improve, downward pressure on the RMB intensifies; the RMB's strategy of closely tracking the U.S. dollar has shifted to a basket-of-currencies model, and clear cyclical fluctuations have already emerged.

Summary: The central bank and the forex bureau have a clear stance: the RMB exchange rate will see a wider fluctuation band, and the era of two-way movement has arrived; China's import and export trade already shows a diversified composition, and behind the large volume of non-USD trade, the strategy has shifted from closely tracking the U.S. dollar toward direct conversion and a trade strategy dominated by a basket of currencies; against other major trade currencies, the RMB, within a 10-year window, is already at a historical strong point, and cyclical fluctuations will become even more pronounced.

III. An Overview of China's Traditional Forex Industry

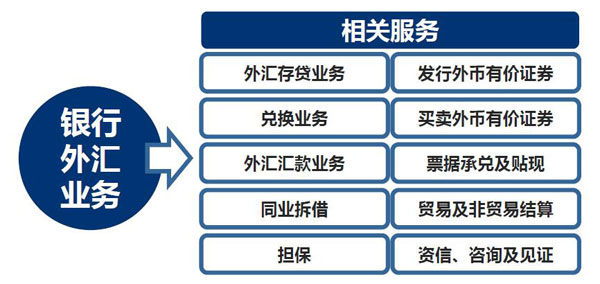

Looking at traditional bank forex business, banks' forex business currently mainly consists of foreign currency deposits and loans, currency exchange, foreign currency remittance, interbank lending, guarantees, and the issuance of foreign currency securities. As the core operating institutions of the traditional forex industry, banks still fall relatively short in the products and services they offer for the forex needs of small and medium-sized institutions and individuals compared with foreign counterparts. In addition, the differentiated services provided by various currency brokers in overseas markets are precisely what form an efficient and convenient service system that divides the market along professional specialization.

Looking at the participation models in China's forex market, banks remain the most important participants. At the China Foreign Exchange Trade System, 30 banks hold interbank forex market maker qualifications, and 26 banks hold RMB forex forward and swap market maker qualifications. Besides banks, China's forex market currently also features two models: small-amount currency exchange, and currency brokerage firms. There were 50 small-amount RMB/foreign currency exchange operators nationwide last year, and the number may exceed 100 this year, but they cannot yet become market mainstays. There are currently only 5 currency brokerage firms nationwide, and their operating scale and market position are negligible. Beyond this, the domestic forex market also includes offline models such as domestic-guarantee/overseas-loan and overseas-guarantee/domestic-loan, offshore forex trading conducted within China, and underground money houses, whose trading volumes are also estimated to be enormous. However, these transactions may fall outside the monitoring scope of the State Administration of Foreign Exchange, making transaction data difficult to compile. Taking Hong Kong as an example, in the first four months of 2013, bilateral trade between the mainland and Hong Kong reached USD 150 billion, up 66% year-on-year from the same period in 2012, whereas in the first four months of this year it was only USD 100 billion, down 33%. Such large swings occurred because arbitrage funds previously inflated trade figures through so-called fake trade; this year the central bank cracked down on hot arbitrage money through RMB depreciation, affecting arbitrage flows, which manifested numerically as a decline in trade volume. Arbitrage flows are conducted through overseas-guarantee/domestic-loan or domestic-guarantee/overseas-loan, involving both onshore and offshore markets, which are not within the purview of the same regulator, making management and statistics very difficult. Because forex trading has not been truly opened in China, using offshore and onshore capital pools and operating cross-border currency through a cross-border capital pool model is also one of the approaches adopted by many domestic and foreign enterprises. In the highly time-sensitive forex market, rapid demand has given rise to these markets that currently cannot obtain licenses or oversight.

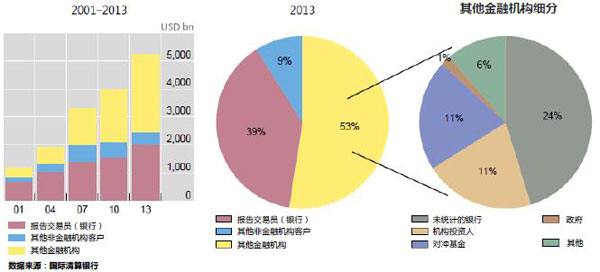

Looking at the types of trading institutions in overseas forex markets, banks account for roughly half of the average daily trading share in the global forex market, with other participants including individuals, enterprises, and institutions. Diversified market participation has also established the forex market as the world's largest, most active, and most transparent trading market.

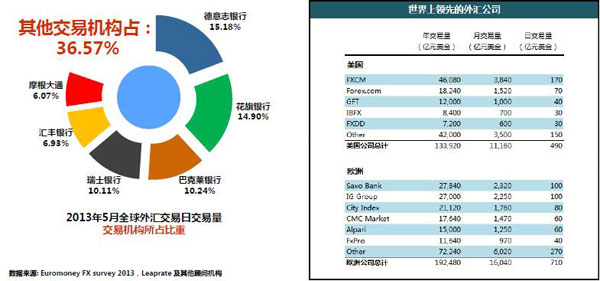

Looking at the trading volumes of banks versus non-bank institutions in overseas forex markets, the world's major trading banks account for over 70% of daily trading share. Specifically, Deutsche Bank has the largest trading volume share, at 15.18%, followed by Citibank, Barclays, UBS, HSBC, and JPMorgan. However, because forex market trading volumes are enormous, the monthly/annual trading volumes of non-bank financial institutions are astonishing. The daily trading volume of just one U.S. forex company, FXCM, reaches USD 17 billion, with monthly trading volume approaching USD 400 billion; Europe's largest forex company, Saxo Bank, also has daily trading volume exceeding USD 10 billion and monthly trading volume of over USD 200 billion. This shows that, besides banks, non-bank trading institutions should constitute an important component of the forex market, and China's forex market needs to strengthen the role and function of non-bank trading institutions in its future development.

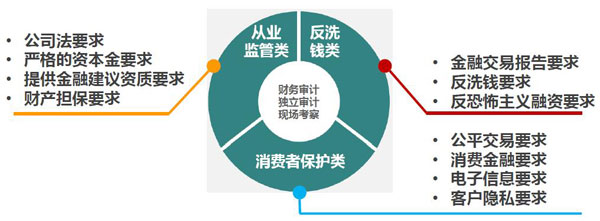

Looking at overseas forex industry regulatory systems, governments' forex industry regulation mainly falls into three categories: practice supervision, anti-money-laundering, and consumer protection. Overseas oversight of financial practitioners is very stringent and protects consumer rights to the greatest extent; compliance requirements for financial institutions and the penalty measures for violations are also extremely strict (e.g., in 2013, HSBC was fined USD 1.9 billion and Deutsche Bank USD 2.3 billion, etc.).

Looking at forex industry regulatory trends, although the markets faced differ, there is a consistent call for improved market regulatory mechanisms. Only under sound competition and regulatory mechanisms can market participants leverage their different strengths and drive the entire industry toward healthy development. Data over the past three years show that the global forex industry's regulatory mechanisms are undergoing further improvement. China's regulators should adopt an open posture on market entry and strengthen ex-post management. Currently, the State Administration of Foreign Exchange's regulatory footprint nationwide is vast, with over 800 regulatory bodies. From top to bottom it is divided into four levels—head bureau, branch bureau, central sub-bureau, and sub-bureau—adopting a model of local jurisdiction with centralized filing. However, core approval authority remains concentrated at the head/branch bureaus, and the administrative management pressure across the four levels has not been effectively dispersed.

Summary: China's traditional forex industry has a relatively simple composition and lacks the participation of non-bank professional brokerage institutions; China's forex demand is growing rapidly, and the market needs diversified products and services to meet enterprise and individual needs; China's forex industry regulation appears vast and stringent, but is unable to effectively manage many industry realities. Here it is necessary to add regulatory categories, shifting from volume control to entry and operational compliance oversight of practitioner institutions, so as to bring current offline forex trading into the light.

IV. Development Prospects for China's Forex Industry and Corporate Response Strategies

1. China's Retail Forex Industry Has Broad Prospects

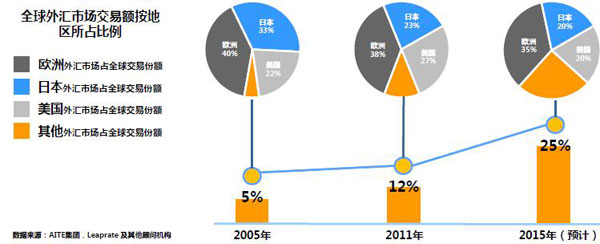

Although, according to statistics from within China, China's monthly trading volume accounts for less than 0.5% of the global total (global average monthly trading volume in 2013 was USD 160 trillion, while China's monthly peak was over USD 700 billion), overseas analytical institutions believe the actual trading volume is far greater than this figure. As shown in the chart below, currently at least over 20% of transactions are generated in non-statistical regions, of which a large portion of the trading volume comes from China.

Looking at the demand population, with the continuous growth of personal income in China, the further diversification of investment channels, and the convenience of outbound travel and other conditions, China's retail forex market already has a huge demand base.

Looking at investment types, although the annual income level of Chinese stock market investors is relatively low compared with the per capita level in Japan, investors' investment scale is relatively high. Moreover, data show that 78.6% of Chinese individual investors participate in stock trading primarily to profit from buy-sell price spreads. For a potentially opening China retail forex market, this represents enormous client potential.

2. China's Corporate Forex Services Industry Remains a Blank

The 2013 foreign trade data released by the General Administration of Customs on January 10 showed that total imports and exports for the year reached USD 4.16 trillion; of this, Guangdong Province's foreign trade volume in 2013 was as high as RMB 1.09 trillion. Traditional banking institutions focus mainly on large institutions for forex finance, cross-border capital pool management, and forex hedging, while various small and medium-sized import and export enterprises nationwide are the main force contributing trillions in trade volume, yet the industry remains a blank, lacking professional institutions and products. It is clear that traditional financial services have not fully covered the enterprises in need, and the financial tools the market offers can hardly meet enterprise needs.

3. The International Sophistication of Professional Forex Systems Urgently Needs to Be Raised

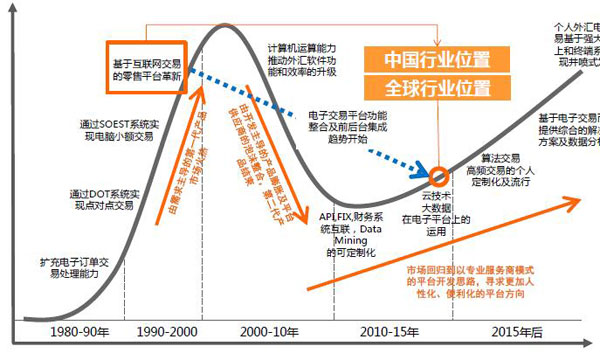

The chart below shows the development status of professional forex systems. Currently, the trend toward functional integration and front-to-back-office consolidation of global forex electronic trading platforms has already begun, and is advancing toward the application of cloud computing and big data on electronic platforms. Yet the construction of electronic trading systems in China's forex industry is still in its infancy, lagging the international industry level by at least 5 years. To raise the international sophistication of China's professional forex systems, it is necessary to introduce non-bank institutional participants, allowing these institutions to conduct business in sync under compliant oversight and to align with international standards.

4. Enterprises Must Build Forex-Related Soft Power

Since both retail and corporate forex demand will experience rapid development, this will be concentrated in several areas: global asset allocation, import and export trade, and cross-border investment and financing. In addition to striving to align with the products and services offered by overseas markets, it is also necessary to further enhance electronic and networked trading functions; attention should be paid to the industry's long-tail effect to form outward-oriented forex supply chain finance.

To greet the advent of China's forex era, enterprises need to build forex-related soft power from various angles. First, in terms of corporate forex trading, independent forex trading and management functional positions should be established to address exchange rate fluctuation risk. A sample survey of 200 overseas enterprises found that 75% of enterprises had established this type of position. Second, in terms of corporate forex management, the internet and electronic trading systems should be used to promote the enhancement of industry products and services, achieving effective internal and external forex trading and risk management systems and protecting profits earned in trade. Third, in terms of system and process enhancement, fully recognize forex risk, achieve efficient trading, management, approval, and supervision work through system platforms, accumulate experience in the process, and enhance comprehensive corporate soft power.

Summary: In China's forex market, both retail and corporate forex demand will experience rapid development. In addition to striving to align with the products and services offered by overseas markets, it is also necessary to further enhance electronic and networked trading functions; attention should be paid to the industry's long-tail effect to form complete forex supply chain finance; enterprises should build forex-related soft power to face the advent of China's forex era.

V. Q&A Session

Q1: How do you view the current RMB exchange rate fluctuations?

A1: The fundamental trend of the RMB this year has not undergone a fundamental change. The central bank intends to push forward exchange rate reform through RMB depreciation and to crack down on arbitrage trading and hot money. The RMB may fluctuate within the 6.15-6.35 range. Unless arbitrage flows or carry trades see a stronger growth trend, no one-way RMB depreciation or appreciation trend is expected this year.

Q2: How do you view the recent changes in the U.S. dollar's trajectory in the market?

A2: Over the past few days, non-USD currencies have appreciated in the market, but the fundamental strength of the U.S. dollar has not changed. The pace of the QE exit will affect the dollar exchange rate to some extent, but essentially there has been no reversal on the technical side. Some say the recent adjustment in the dollar index is due to the technical flow of certain positions or products. It is still too early to conclude that the dollar is weak.

Q3: Recently the spread between the RMB spot rate and forward rate has been narrowing, with the spot rate even depreciating more than the forward rate. How do you interpret this?

A3: The occasional occurrence of an inversion between the spot rate and the forward rate in the short-term market is a matter between these two markets, and it is precisely the purpose of the central bank's intervention in the RMB exchange rate—namely, to make investors aware that an imbalance in supply and demand can cause an inversion of the exchange rate between the two markets and thereby bear arbitrage costs.

Q4: How do you view the regulators' move to open many channels while cracking down on cross-border arbitrage?

A4: Recently, many Hong Kong enterprises have been issuing bonds to increase their foreign currency scale, which is largely related to funding demand within the mainland. At the same time, the Shanghai Free Trade Zone is also liberalizing cross-border capital settlement between offshore and onshore capital pools. On one hand, the central bank is promoting the construction of market elements such as channels and tools; on the other hand, cracking down on arbitrage is the central bank's long-term regulatory objective. Although in the short term the two occasionally diverge, in the long term this is not an either-or issue. Once market elements become abundant, the central bank will still spare no effort to crack down on arbitrage activity.

[Continued in column I]